![Is It Still a Seller's Market? Here's What the Data Says. Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us. While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again. And that balance is something we haven’t had in a while. Whether you're buying or selling, here's what you need to know about what's changing and what it means for your move. The Most Buyer-Friendly Market in YearsThe national data tells an interesting story right now. According to Realtor.com: "The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . ." That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below). Back in 2021, almost all major metros were seller's markets. By the end of 2025, only 1 in 3 still favored sellers. That's an obvious shift. And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking. It’s Not the Same Story EverywhereThat said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller's markets right now, too. It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region. Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn't see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains: “The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.” Practical Advice for Your MoveTo find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move. If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market. Here's some practical advice if there’s a mismatch between your goal and local market conditions. If you're buying in a seller's market: - Get pre-approved before you start shopping. It shows sellers you're serious. - Be ready to act fast when the right home hits the market. - Consider offering a quick closing date or flexible terms. - Work closely with your agent to craft a competitive offer. If you're selling in a buyer's market: - Price it right from day one. Overpricing will cost you time and money. - Focus on curb appeal and staging to stand out in areas with more inventory. - Be open to offering incentives, like covering closing costs or a home warranty. - Expect buyers to negotiate and be ready to be flexible. Bottom LineRight now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market. Is It Still a Seller's Market? Here's What the Data Says.](https://alstonhomes.com/wp-content/uploads/6-18-26-218x150.png "Is It Still a Seller’s Market? Here’s What the Data Says.")

If you’re worried about a coming recession, you’re not alone. Over the past couple of years, there’s been a lot of recession talk. And many people worry, if we do have one, it would cause the unemployment rate to skyrocket. Some even fear that a spike in unemployment would lead to a rash of foreclosures similar to what happened 15 years ago.

However, the latest Economic Forecasting Survey from the Wall Street Journal (WSJ) reveals that, for the first time in over a year, less than half (48%) of economists believe a recession will actually occur within the next year:

“Economists are turning optimistic on the U.S. economy . . . economists lowered the probability of a recession within the next year, from 54% on average in July to a more optimistic 48%. That is the first time they have put the probability below 50% since the middle of last year.”

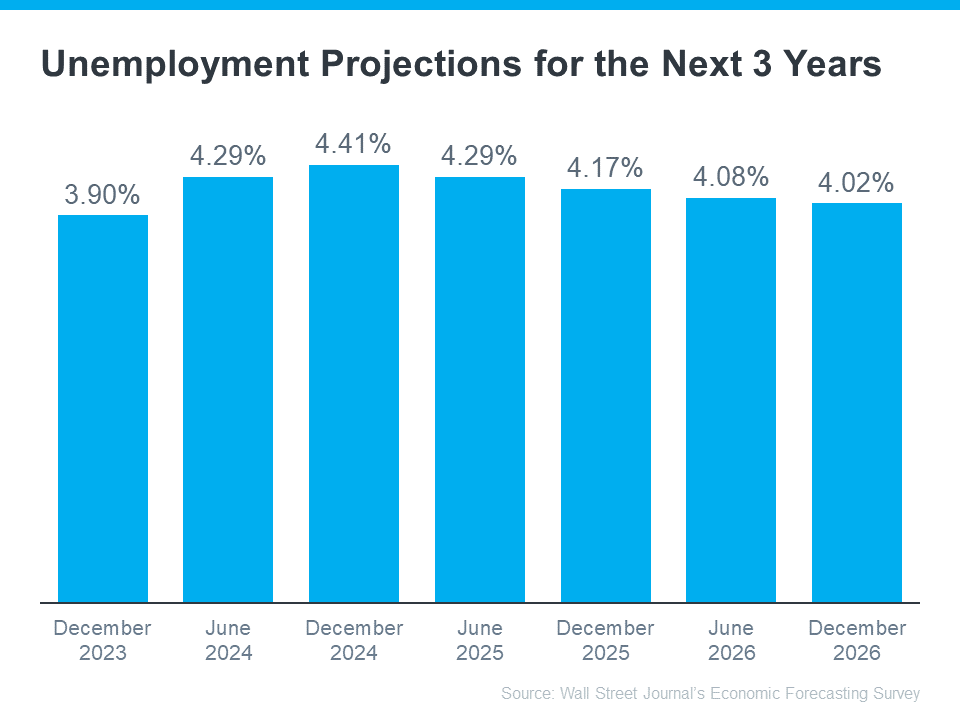

If over half of the experts no longer expect a recession within the next year, you might naturally think those same experts also don’t expect the unemployment rate to jump way up – and you’d be right. The graph below uses data from that same WSJ survey to show exactly what the economists project for the unemployment rate over the next three years (see graph below):

If those expert projections are correct, more people will lose their jobs in the upcoming year. And job losses of any kind are devastating for those people and their loved ones.

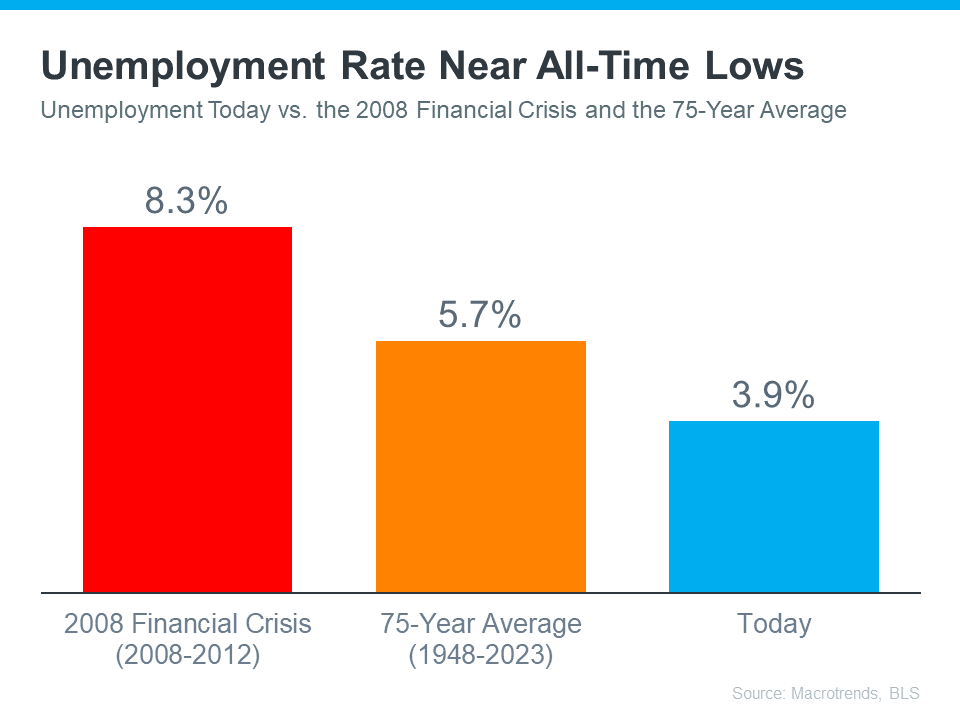

However, the question here is: will there be enough job losses to cause a wave of foreclosures that will crash the housing market? Based on historical context from Macrotrends and the Bureau of Labor Statistics (BLS), the answer is no. That’s because the unemployment rate is currently near all-time lows (see graph below):

As the orange bar in the graph shows, the average unemployment rate dating back to 1948 is 5.7%. The red bar shows, the last time the housing market crashed, in the immediate aftermath of the 2008 financial crisis, the average unemployment rate was up to 8.3%. Both of those bars are much higher than the unemployment rate today (shown in the blue bar).

Moving forward, projections show the unemployment rate is likely to stay beneath the 75-year average. And that means we won’t see a wave of foreclosures that would severely impact the housing market.

Bottom Line

Most economists no longer expect a recession to occur in the next 12 months. That’s why they also don’t expect a dramatic rise in the unemployment rate that would lead to a rash of foreclosures and another housing market crash. If you have questions about unemployment and its impact on the housing market, let’s connect.

{kind=link}